Tom Lee: Doesn't Believe in Crypto Winter in the Near Future, ETH Long-Term Target $60,000

The Best-Haired Man on Wall Street Analyzes the $8 Billion ETH Bet Logic.

Original Title: Medici Level Up with Tom Lee, Chairman of BitMine

Original Source: Medici Network

Original Translation: Azuma, Odaily Planet Daily

Editor's Note: What was the strongest buying force behind ETH's current rally? The answer lies in none other than the ETH Treasury Company. With the continuous accumulation of BitMine (BMNR) and Sharplink Gaming (SBET), the narrative power of ETH has quietly shifted — for more details, please refer to "Unveiling the Two Key Figures Behind ETH's Rally: Tom Lee VS Joseph Rubin".

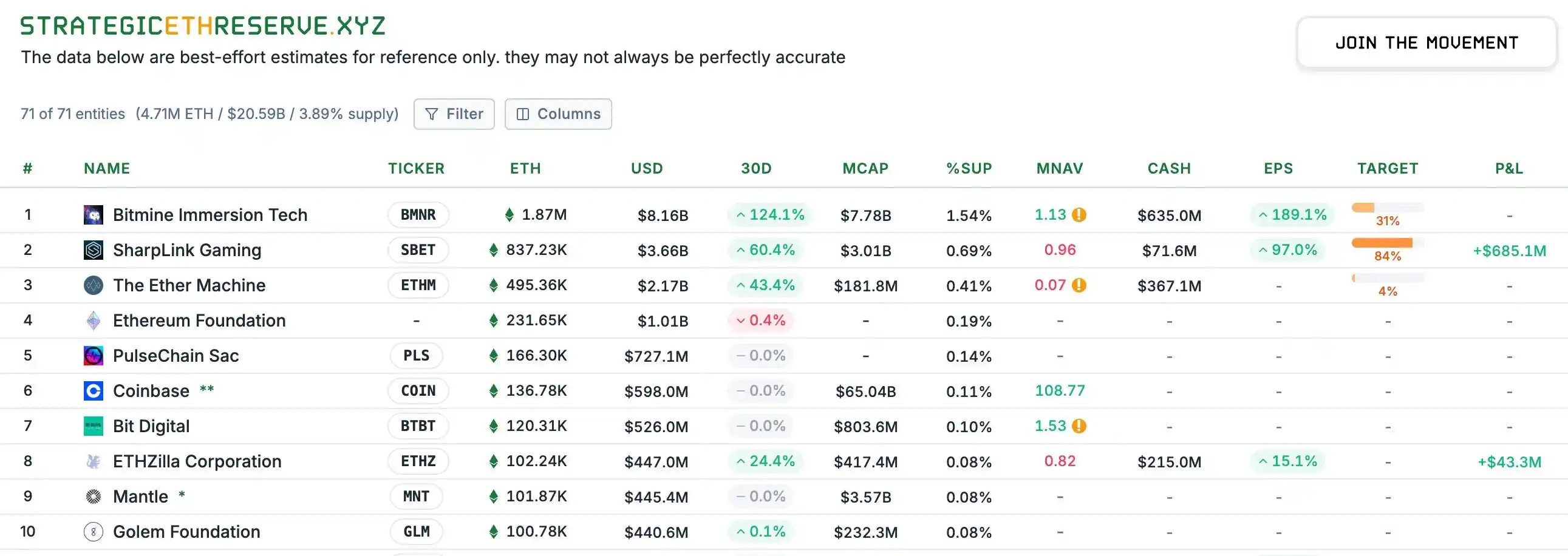

According to Strategic ETH Reserve data, as of September 4th Beijing time, BitMine's ETH holdings have reached 1.87 million coins, worth approximately $8.16 billion. Tom Lee, the helm of BitMine, has long been the most influential whale in the current Ethereum ecosystem.

On the evening of September 3rd, Tom Lee participated in an interview on the podcast show Level Up under Medici Network. In the conversation, Tom Lee discussed ETH's position in the global financial arena, BitMine's rise as a leader of the ETH treasury, and the macro environment surrounding digital assets. Tom Lee also shared his views on the long-term potential of cryptocurrency, the vision of decentralization, and BitMine's plans to further increase its reserve size.

Below is the original interview content, translated by Odaily Planet Daily — for the sake of readability, some content has been edited for brevity.

· Host: Could you briefly tell us your story? How did you enter the cryptocurrency market? (When introducing Tom Lee, the host not only mentioned his usual title, but also referred to him as the "Wall Street's most handsome man.")

Tom Lee: In short, after graduating from college (at the Wharton School), my entire career has basically only had one job, which is market research. I started my career at Kidder, Peabody & Company, researching the tech industry, particularly wireless communications, from 1993 to 2007.

That experience taught me some important lessons. Wireless communication was still in its early stages back then — there were only 37 million mobile phones globally, whereas today it's close to 8 billion, showing exponential growth. However, what surprised me was that many customers at that time were actually very skeptical of wireless technology. In their view, the core business of the telecom industry back then was long-distance and local phone calls, and mobile phones were just "upgraded wireless phones" that might eventually become free.

So, I realized at that time: "Fund managers in their forties and fifties often fail to truly understand technological disruption because they are essentially vested interests." After that, I became the Chief Strategic Officer at J.P. Morgan, holding the position until 2014. Later on, I founded Fundstrat with the goal of establishing the first Wall Street company to attempt to "popularize institutional research" — that is, to open up research that was originally only available to hedge funds and large asset managers to a broader audience. We hoped to make research services that were originally provided to hedge funds and large institutions available to the public.

Then, around 2017, I began to notice news about Bitcoin surpassing $1,000. This reminded me of my time at J.P. Morgan's foreign exchange team when we had discussed Bitcoin on several occasions. Back then, the price of Bitcoin was less than $100, and the core of the discussion was whether this digital currency could be recognized as a form of money.

However, at J.P. Morgan, the attitude was very negative, viewing Bitcoin as nothing more than a tool for drug dealers and smugglers. But in my twenty-year career at the time, I had never seen an asset rise from under $100 to $1,000, and its market cap surpass $10 billion. This was definitely something that could not be ignored, and I had to research.

So, we began our research. Although I couldn't fully understand why the "Proof of Work blockchain" could become a store of value at that time, I found that just two variables could explain over 90% of Bitcoin's surge from 2010 to 2017: wallet count and each wallet's activity.

Based on these two variables, we could even model and speculate on Bitcoin's potential future trends. This was my first true "journey" into the crypto space. So, when the price of Bitcoin was still below $1,000, we released the first white paper. We proposed: if someone were to consider Bitcoin as an alternative to gold, and it only held a 5% share of the gold market, then the fair price of Bitcoin would be $25,000. This was our prediction for the price of Bitcoin in 2022 at the time, and by 2022, Bitcoin's price indeed hovered around $25,000.

· Host: You just talked about BTC, but you are also doing some very interesting things on ETH. Can we discuss the macro opportunity of ETH?

Tom Lee: For a long time, roughly from 2017 to 2025, our core view in the crypto space has been that Bitcoin occupies a very clear position in many people's portfolios, not only because it has been validated in terms of scale and stability, but more importantly because it can serve as a store of value.

When we think again about how investors should allocate in crypto assets beyond Bitcoin, there are many projects out there—such as Solana, Sui, and various projects you often write about. But starting from this year, we are seriously re-evaluating Ethereum.

The reason is: I believe that this year the regulatory environment in the United States is moving in a favorable direction, which is causing Wall Street to take cryptocurrency and blockchain more seriously. Of course, the real "killer app" or the so-called ChatGPT moment is actually stablecoins and Circle's IPO, followed by the Genius Bill and the SEC's Project Crypto initiative.

I see many bullish factors for ETH here, but the main point is—as we observe the asset tokenization projects that Wall Street is advancing, whether in dollars or other assets, the vast majority are happening on Ethereum.

What's more important is that I think people need to take a step back: what is happening on Wall Street in 2025 is very much like the historical moment of 1971. In 1971, the US dollar was detached from gold, abandoning the gold standard. Back then, gold did benefit, and many people bought gold, but the real core was not the gold benefit, but that Wall Street opened up financial innovation—because suddenly, the dollar became fiat currency, no longer backed by gold, and people had to establish new circulation and payment "tracks" for dollar transactions. Therefore, the real winner was Wall Street.

By 2025, the innovation brought by blockchain is solving a lot of problems, and Wall Street is moving to the crypto "track," which, in my view, is ETH's "1971 moment." This will bring huge opportunities to migrate a large amount of assets and transactions to blockchain. Ethereum will not be the only winner, but it will be one of the primary winners.

From an institutional adoption perspective, I've heard a lot of relevant discussions. BTC has become very institutionalized. When I meet with investors, they all know how to build models, how to think about BTC's future value. So, BTC has entered many portfolios. In contrast, ETH's holding rate is still very low, more like BTC in 2017.

I believe that ETH is not yet truly seen as an "institutional asset" today, so it is still in a very early stage, which is also why I think ETH has a greater opportunity.

· Host: I know you have set a target price for Ethereum, roughly around $60,000, how did you make this prediction?

Tom Lee: Yes, that's right. But I have to clarify, ($60,000) this is not a short-term target. So, don't come at me on December 31st saying "it didn't go up that much," this is not the kind of prediction that will be fulfilled next week.

In fact, what I was quoting at the time was an analysis we did for ETH, which was done by Mosaics and some other researchers. Their idea was to treat the present as a turning point similar to 1971. They thought about Ethereum's value from two perspectives: one as a payment rail and the other as a portion of the payment market share Ethereum can occupy, and I think these two concepts can be overlapped.

Their vision is that if you look at the market covered by the banking system and assume that half of it will move to the blockchain, then Ethereum could capture about $38 trillion in value; then you look at Swift and Visa, they can process about $450 billion in payments each year, if you assume that each transaction will incur a Gas fee and convert it to network revenue, and give it a relatively conservative 30x P/E ratio, you end up with an estimated value of about $3 trillion. Adding these two parts together, Ethereum's fair valuation should be around $60,000, which means there is still roughly an 18x growth potential from now.

· Host: Recently, much of ETH's bullish sentiment has been linked to continued buying by digital asset treasury companies. As the Chairman of BitMine, how do you think investors should consider different investment paths, such as choosing between ETFs, spot, and treasury company stocks?

Tom Lee: First of all, if someone wants to get ETH exposure through an ETF, that's totally fine because it allows you to invest in ETH directly without much price difference, just like the BTC ETF, giving you direct BTC exposure.

However, if you look at BTC treasuries, companies like MicroStrategy have a larger holding than the largest BTC ETF. In other words, compared to an ETF, more investors are willing to indirectly hold BTC through MicroStrategy. The reason is simple: treasury companies do not just offer you a static ETH holding; they actually help increase the amount of ETH per share you own. MicroStrategy is a prime example: when they pivoted to a BTC strategy in August 2020, their stock was around $13, and it has now surged to $400, a thirty-fold increase over five years, while BTC itself has risen from $11,000 to $120,000 in the same period, an eleven-fold increase. This shows that MicroStrategy has successfully increased the amount of BTC per share held, while BTC ETFs have remained static during this time.

In other words, while an ETF might have made you earn eleven times your investment in five years, MicroStrategy's treasury strategy enables investors to earn even more. They leverage stock liquidity and volatility to consistently increase the BTC holdings per share. This is precisely Michael Saylor's strategy, where from initially having 1 to 2 dollars' worth of BTC per share, it can now correspond to $227, a significant increase.

· Host: You just mentioned that traditional investors' interest in Ethereum is increasing. I'm curious, over the past few months, have you noticed any changes in the attitudes of some non-crypto-native institutional clients when discussing treasury companies with them?

Tom Lee: To be frank, most people are quite skeptical when considering crypto treasuries. Indeed, many who invested in MicroStrategy have made good profits, but even so, its shareholder base is not as extensive as you might think because there are still many institutions that simply do not believe in cryptocurrencies. For example, a recent survey by Bank of America showed that 75% of institutional investors have zero exposure to crypto. This means that three-quarters of people have not touched crypto assets at all. So when they see treasury companies, their initial reaction is, "Why not just buy the tokens directly?"

Thus, we've spent a lot of time educating them at meetings. Using BitMine's data as an example, the difference lies in the fact that treasury companies can help increase the amount of ETH per share you own. For instance, when we transitioned to an ETH treasury on July 8th, each share only corresponded to $4 worth of ETH, and by the update on July 27th, each share was equivalent to $23 of ETH, nearly a sixfold increase in just one month. This disparity is significant and illustrates the "per-share ETH acceleration effect" brought about by a treasury strategy.

· Host: There are many ETH treasury companies in the market, but obviously BitMine has been the quickest to act. How did you manage to do that?

· Tom Lee: I think MicroStrategy provided a good template. The first BTC treasury company was actually Overstock, but it didn't really resonate with investors, and the stock price didn't benefit. Saylor was the first person to approach this in a more scalable and systematic way, which truly inspired us. So our strategy at BitMine is to maintain an extremely clear and concise path, relying solely on common stock to operate, avoiding complex derivative structures, making it easy for investors to understand at a glance. In the future, we may consider strategies involving volatility or market capitalization, but the first step is to have a clear strategy that shareholders can trust.

Why is this important? Because investors need to believe that what they're buying into is not just ETH, but a long-term macro trading opportunity. Companies like Palantir can command a premium valuation not only because of their product but also because shareholders feel they hold something "meaningful." Our goal is to help investors understand that Ethereum is indeed one of the biggest macro trading trends of the next 10–15 years.

· Host: Speaking of the premium topic for treasury companies, Michael Saylor has said that he would more actively use ATM (at-the-market) offerings within a premium range of 2.5 to 4 times NAV (Net Asset Value). I think among all treasury companies, you have been more aggressive in increasing NAV through ATM, right? Even willing to do so at lower premium levels, yet you have achieved consistent and robust NAV growth. How do you consider the appropriate premium multiple? Like Saylor mentioned, he is at one extreme, believing it's not worth aggressive action unless it's below 4 times. What's your perspective?

Tom Lee: I think there's a strange math problem here.

In theory, every financial instrument requires a certain balance—this may be a bit technical for the audience—common stock is actually a good financing tool because it provides everyone with equal upside potential without conflicts of interest—both existing and new shareholders are betting on the company's future success.

But when you finance with convertible bonds, the situation is different. Buyers not only care about the stock price but also seek to capture volatility, and may even eliminate volatility through hedging. Preferred stock and debt are essentially liabilities—although ETH treasury companies can pay off debt through staking rewards, that financing is still debt. Debt holders don't care about the company's success; they only care about interest payments.

So, if you introduce conflicting motivations and different incentive measures when changing your capital structure, you might actually harm the company—too many convertible bonds can suppress volatility, thereby hindering the flywheel effect (volatility is indeed the foundation of stock liquidity).

Therefore, it is challenging to precisely calculate the intervals for grade operations. Another point to keep in mind is—in the next crypto winter (which is inevitable), companies with the simplest balance sheets will prevail. This way, you won't have to discount financing obligations, nor will you end up with a natural short position due to derivative structures—when the stock price falls, more short selling is triggered due to coverage requirements, creating a death spiral. This is why Bitmine maintains a simple structure.

If a treasury company's premium is only slightly above NAV by 10%, it is challenging to rationalize ATM operations—based on mathematical calculations, when issuing stock at a 1.1x premium, you need to sell 100% of outstanding shares (doubling the total shares outstanding) to have a positive impact on ETH holdings per share. However, if you operate at a 4x premium, you only need to sell 25% of shares to double the ETH holdings per share. I guess Saylor's logic is in this, but my approach is different. I think a more strategic mindset might be better.

· Host: You mentioned the inevitability of a downturn cycle. We have experienced several crypto winters. What do you think the impact will be on treasury companies?

Tom Lee: It's hard to say, but the best analogy is probably the oilfield service industry. The simplest analogy for cryptocurrency treasury companies is oil companies. Investors can buy oil, buy oil contracts (or even physical delivery), but many people buy oil company stocks, such as ExxonMobil or Chevron, which always trade at a premium to proven reserves, because these companies are actively acquiring more oil.

When the capital market turns unfriendly, companies with more complex capital structures will collapse. During a crypto winter, valuation gaps will be greater, and companies with the cleanest balance sheets can acquire assets, possibly even trading at a discount to net asset value.

· Host: Are you suggesting that there may be some mergers/integrations among treasury companies?

Tom Lee: Yes, the folks at Bankless once made a great point. They said that in the Bitcoin treasury race, MicroStrategy is clearly way ahead, but in the Ethereum treasury race, there is currently no absolute leader. As of now, everyone can still easily obtain funding, so it's not yet time for necessary integration.

If there is indeed going to be integration, I think it is more likely to happen in the Bitcoin Treasury market, because Bitcoin has already experienced a significant price surge (although I am still bullish and believe it can reach $1 million), but Ethereum is still in the early stages of realizing its value. So, the scenario you just described, I think is more likely to occur on top of Bitcoin.

· Host: You mentioned earlier about maintaining a clean balance sheet. In a crypto winter, if the company's stock price is trading at a discount, would you consider stock buybacks? Would this be achieved through issuing debt or by keeping additional cash reserves outside of the ETH position?

Tom Lee: That's a good question, but we can only discuss it at a theoretical level. Firstly, I do not believe we will see a crypto winter in the near future. Clearly, we are still bullish on the market, so I do not anticipate a winter anytime soon. Of course, it will happen at some point in the future, and at that time, BitMine will have several sources of cash flow:

First, from our traditional core business;

Second, from staking rewards, as staking returns can be converted into fiat when needed for buybacks, theoretically achieving up to a 3% buyback scale, which is already significant;

Third, considering whether to use the capital markets to support buybacks.

At that time, companies with the cleanest balance sheets will be able to do a lot. For example, using ETH as collateral for loans, the market interest rate is known, so there are many ways to do this, but each company's approach will be different in practice. If the balance sheet is complex, it is basically impossible to self-insure during a discount.

· Host: To keep BitMine's stock price above its NAV, would you consider mergers and acquisitions? Because this way, from a per-ETH perspective, value is added. At what discount level do you think mergers would make sense?

Tom Lee: I think each company has its own algorithm. If a company's stock price cannot exceed NAV even in a scenario where ETH still has significant room to rise, then it is merely following the Beta exposure of ETH. On the other hand, those companies that can obtain a premium must make Alpha choices. In other words, you can buy more ETH to get the Beta exposure, but if you want to outperform it, you must have an Alpha strategy.

The reasons for each company's discount may also vary, such as poor liquidity, high debt, complex business operations, etc., all of which can lead to a justifiable premium or discount.

· Host: Changing the topic a bit, although not directly related to BitMine, I'd like to ask, do you think MicroStrategy will be included in the S&P 500 in September?

Tom Lee: The workings of the S&P 500 committee are confidential, but they do a good job. If you look at historical data, every 10 years, over 20% of the index's returns come from companies that were not in the index ten years ago. In other words, they (S&P 500) are actually actively selecting stocks based on themes rather than mechanically following rules.

In fact, their performance is much better than a total market index like the Wilshire 5000 and even better than the Russell 1000 (by market cap weight). This indicates that they are not just selecting the largest companies but are making thematic judgments. AI is certainly a focus, Crypto is also key, and they will consider reducing the weight of commodities-sensitive holdings.

· Host: Speaking of indices, BitMine is growing rapidly, is there a possibility of being included in some indices?

Tom Lee: It is currently not possible to be in the S&P series because it requires positive net income, which we can achieve after starting native staking. The Russell index is quantitative, looking only at trading volume and free float market cap. The threshold for the Russell 1000 is around $5 billion, with a restructuring period every June. Starting in 2026, this will change to every six months. By that standard, BitMine has far exceeded the threshold.

· Host: I think we've covered a lot in our discussion today. It's been a great conversation. Do you have any final thoughts or key points you'd like to leave with the audience?

Tom Lee: I'd like to summarize: we are actually witnessing a historic moment in the financial industry. Because blockchain has solved many problems, democratizing finance, breaking the previous gatekeeper structure of controlling resources. Even when discussing universal basic income, blockchain and cryptocurrency can provide solutions. So, I believe we should not only be optimistic about the short-term prices of Bitcoin and Ethereum but also see their profound positive impact on society.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Cathie Wood Revises Bitcoin’s 2030 Forecast: Will Stablecoins Take Over?

In Brief Cathie Wood revises Bitcoin's 2030 target due to rapid stablecoin adoption. Stablecoins serve as digital dollars, impacting Bitcoin's expected role. Trump's crypto-friendly policies encourage Bitcoin's market prominence.

Internal Conflict Sparks Unanticipated Surge in FET Value

In Brief ASI faces internal conflict amid legal battles impacting future prospects. Surprisingly, lawsuit news boosted FET buying interest and trading volume increased. Potential for renewed interest in AI-themed tokens as investors watch developments.

Altcoins Signal a Paradigm Shift: How the Crypto Landscape is Shaping Up

In Brief A new altcoin season might be approaching, signaling significant market shifts. US monetary policy actions could influence the rise of altcoins. Increased trading volumes in Asia highlight global interest in altcoins.

Polymarket Rebounds With Growing User Activity as Wash Trading Concerns Rise