Global Economic Weekly Outlook: Ahead of the Federal Reserve Meeting, U.S. Job Growth Expected to Slow Down

In August, U.S. employers showed weak hiring intentions, and the unemployment rate may rise to its highest level in nearly four years, further confirming the decline in labor market activity.

According to the median data from surveys, economists expect about 75,000 new jobs to be added in August, with the unemployment rate reaching 4.3%. If the number of jobs added for four consecutive months remains below 100,000, it will mark the weakest growth cycle since the early days of the 2020 pandemic.

Weak Growth in the U.S. Labor Market:

The employment data released by the U.S. Bureau of Labor Statistics on Friday will serve as a key reference for Federal Reserve officials ahead of the September policy meeting. Some officials are less concerned about the slowdown in job growth because the labor force participation rate is also declining; in addition, current inflation is gradually rising, so they remain cautious about cutting interest rates.

However, other officials (such as Federal Reserve Governor Waller) have stated that the slowdown in hiring in recent months means the Fed should proceed with the first rate cut of the year.

In the coming week, even though the employment report has not yet been released, investors will still pay attention to speeches by several Federal Reserve officials, including St. Louis Fed President Alberto Musalem, New York Fed President John Williams, and Chicago Fed President Austan Goolsbee. The Fed will also release the beige book on Wednesday, summarizing economic observations from across the country.

As companies focus on controlling costs (such as coping with higher import tariffs), hiring demand has gradually weakened. Another set of data scheduled for release on Wednesday is expected to show that the number of job vacancies in July declined from the previous month, possibly falling to one of the lowest levels since 2021.

To accelerate job growth, U.S. President Trump is attempting to reverse the trade imbalance, stimulate long-term investment, and promote domestic production of key goods and raw materials through tariff policies.

In the upcoming holiday-shortened week (note: a week with fewer working days due to holidays), other data to watch include the Institute for Supply Management (ISM) manufacturing and services Purchasing Managers' Index (PMI) for August. Government data released on Thursday may show that the trade deficit in goods and services widened significantly in July—preliminary data previously indicated a surge in imports before tariffs were raised.

Canada will also release employment data, and it is expected that the Canadian labor market will remain weak in August amid trade tensions. Data released on Friday showed that trade setbacks have led to Canada's first economic contraction in nearly two years.

Decline in Exports Leads to Contraction in Canadian GDP

Canada's goods trade data for July may show that although exports are slowly recovering from a three-year low in April, the trade deficit will remain high and persistent.

In addition, inflation data from the Eurozone to Turkey, key testimonies from UK policymakers, and economic activity data from across Asia will be highlights of the global economy this week.

Asia

This week will be data-intensive for Australia and South Korea, with multiple releases including second-quarter GDP. Economists expect data to be released on Wednesday to show that Australia's economic growth accelerated in the second quarter, while South Korea's economy remained flat.

Australia will also release second-quarter inventory and building permit data on Monday, and export and household spending data on Thursday. South Korea will release export data on Tuesday (with August export activity expected to slow) and the consumer price index (expected to decline month-on-month).

Thailand and Vietnam will also release Purchasing Managers' Index (PMI) data.

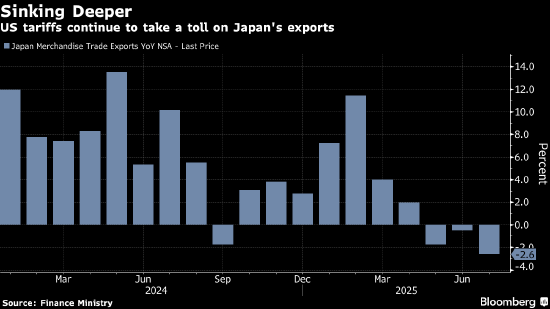

Japan will release second-quarter capital expenditure and corporate profit data on Monday, and will also publish July cash earnings and household spending data later in the week.

Indonesia and Thailand will release consumer price data, and the Philippines will also announce inflation data. As inflationary pressures are gradually easing, these data are expected to show that prices remained stable or declined month-on-month during the month.

In addition, Singapore will release retail sales data on Friday. Malaysia's central bank is expected to keep its interest rate unchanged at 2.75% on Thursday.

Europe, Middle East, and Africa

The Eurozone will release multiple data this week: unemployment rate on Monday, inflation data on Tuesday, and revised GDP on Friday. These data will be released under new rules—media will no longer have early access to information before the official release.

Last Friday, the economic data of the four major Eurozone economies (note: usually referring to Germany, France, Italy, and Spain) were mixed. Economists expect the inflation data to be released this week to be slightly above the European Central Bank (ECB)'s 2% target. This may give officials, who are already prepared to keep rates unchanged at the September 11 meeting, more confidence.

European Inflation Has Not Raised ECB Concerns

On Monday, ECB Executive Board members Isabel Schnabel and Piero Cipollone will chair a panel discussion at the 2025 ECB Legal Conference in Frankfurt, and ECB President Lagarde will deliver a dinner speech.

On Wednesday, Lagarde will also speak as Chair of the European Systemic Risk Board (ESRB); on Thursday, Cipollone will testify before lawmakers in Brussels. Policymakers will enter a "quiet period" on Thursday ahead of the policy meeting (note: a period before policy meetings during which officials refrain from public comments on the economy and monetary policy).

Among the data from Eurozone countries, Germany's factory orders may attract attention—as this data can serve as an early signal of the impact of U.S. tariffs on manufacturing.

Inflation will be the focus across the region:

- Wednesday: Turkey's annualized inflation rate for August is expected to decline, but will still remain above 30%. If there are signs that inflationary pressures are easing, the Turkish central bank may be able to cut rates further.

- Thursday: Switzerland's August inflation rate is expected to remain above zero for the third consecutive month—this is the last inflation report before the Swiss National Bank (SNB)'s quarterly rate decision in September.

- Same day: Sweden will release inflation data. Analysts expect the CPIF inflation index (consumer price index including fixed interest rate housing costs), which is monitored by the Riksbank, to rise to its highest level since early 2024.

The Bank of England Has Lowered Rates to a Two-Year Low

In the UK, testimony from Bank of England officials in Parliament on Wednesday will be a highlight of the week. This month's rate decision vote saw an unprecedented split, and policymakers with differing views (including Governor Andrew Bailey) all plan to speak. Retail sales data will be released on Friday.

Latin America

Mexican President Sheinbaum will announce the opening of the annual parliamentary session on Monday. The economic priorities mentioned in her speech will be closely watched.

Brazil will release second-quarter GDP data on Tuesday, with economic growth expected to slow. Although Brazil's economy may achieve 16 consecutive quarters of expansion, its quarter-on-quarter growth rate is expected to be 0.4%, and year-on-year growth 1.9%, both lower than previous data.

Other data: Chile will release July economic activity data on Monday, expected to grow 2.2% year-on-year; Peru will release August inflation data on the same day. Colombia will release inflation data on Friday, with surveys showing analysts expect its annualized inflation rate to rise above 5%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin News Today: Meme Coin Meets DeFi: PEPETO Builds a Real-World Playbook

- PEPETO, an Ethereum-based meme coin, is positioned as a 2025 bull run contender with real-world DeFi tools like PepetoSwap and audited smart contracts. - Its $6.4M presale and 42 trillion tokens staked (237% APY) highlight strong retail/institutional demand and market confidence. - PEPETO outperforms peers like BlockDag and Bitcoin Hyper through live cross-chain solutions and a 30% staking rewards allocation. - Tokenomics prioritize fairness (no team wallets) and growth, with 100K+ community members and

PARTI +16.36% in 24H Driven by Strong Short-Term Momentum

- PARTI surged 16.36% in 24 hours, 137.97% weekly, and 63,480% annually, showing extreme short- and long-term bullish momentum. - Technical indicators like RSI and MACD confirm sustained buying pressure, with price above key moving averages reinforcing upward bias. - A backtesting strategy using overbought RSI and expanding MACD histograms aims to capitalize on continued momentum in simulated trading.

XRP’s Imminent Breakout: A Confluence of Technical, Institutional, and Regulatory Catalysts

- SEC's 2025 reclassification of XRP as a digital commodity removed regulatory barriers, triggering 176% trading volume surge and unlocking institutional capital flows. - Technical analysis shows XRP testing $3.31–$3.65 resistance, with a $3.65+ breakout potentially driving 65% gains to $5.53 via Fibonacci extensions and golden cross patterns. - Ripple's institutional infrastructure upgrades and $25M/daily inflows from banks transformed XRP into a utility token, aligning with 2017–2018 cyclical patterns th

Bitcoin’s September 2025 Volatility: A Short-Term Downturn or a Setup for a Q4 Rally?

- Bitcoin’s 2025 September volatility sparks debate: short-term correction or Q4 rally setup? - Historical "Red September" trends and institutional adoption suggest a 20–30% correction risk but 70% chance of a 44% Q4 rebound. - Fed rate cuts and dollar weakness could drive Bitcoin toward $160,000 by year-end if institutional flows accelerate. - Technical analysis shows support above $102,200 could break the "Red September" cycle, with a 59% win-rate for holding support levels. - Strategic positioning requi