[Long English Thread] A Brief Analysis of DATs: Financial Engineering or Business Operations? Which is Better, BTC or ETH?

Chainfeeds Guide:

DAT is a financial product, similar to insurance companies and banks, and must balance assets and liabilities.

Source:

Author:

Mippo

Opinion:

Mippo: First of all, I still think that the structure of DAT is mostly "foolish." However, I am increasingly inclined to believe that the existence of many suboptimal structures in the crypto industry is more a result of excessive regulation. So, although I don't think DAT is excellent, I understand the reason for their existence and also believe they will persist for some time. Recently, I read an article written by Denny Galindo and Jane Yu Sullivan from Morgan Stanley. They pointed out that while most people compare DAT to closed-end funds (such as GBTC), it can also be likened to REITs (Real Estate Investment Trusts), insurance companies, or even banks. For me, the core point of the article is: investment vehicles like REITs, insurance companies, and banks have two sources of income: financial engineering—generating returns through market volatility; and operating income—profits from actual business operations. These companies must all balance assets and liabilities. Banks, insurance companies, etc., need to ensure their books can cover customer withdrawals or insurance payouts. Therefore, they prefer highly liquid, income-generating assets (such as government bonds). Insurance companies also have some unique features: their income includes both financial engineering (timing the sale of volatility and balance sheet structuring) and operating income (underwriting income). This is highly relevant when comparing to DAT. In my view, DAT is more like an actively managed financial product (unlike passive products such as ETF). If they can generate higher returns than the underlying assets, they have value, and this highly depends on how much yield they can create. However, at this stage, investors don't really care where these returns come from. For example, Strategy (the company) has come up with some confusing metrics (such as accretive dilution), but essentially, the returns all come from financial engineering. For instance, when bitcoin volatility rises, Saylor can package BTC into different financial structures (convertible bonds, preferred shares, common shares, etc.) and achieve "selling 1 dollar of bitcoin for 2 dollars of valuation." But now, bitcoin's volatility is structurally declining, which is important—because it means Saylor will no longer be able to create more returns through volatility, and this is a big problem for DAT. So my conclusion is: perhaps in the next 2–3 years, investors will gradually begin to distinguish the sources of DAT's returns. If the returns only come from financial market arbitrage, this model's lifespan is limited. But if the underlying assets themselves can generate returns (such as staking rewards), that will be a more sustainable source. This is also why I believe "productive assets" like ETH or SOL have a huge advantage. These chains can not only generate execution layer rewards through real on-chain business activity, but also participate in DeFi (such as lending pools on Aave, Morpho), helping DAT obtain better financing conditions. I have always firmly believed that the structural advantage of ETH and SOL over BTC is that they can generate yield. I am a believer in productive assets. And if DAT continues to dominate market price trends, then this yield stream will be crucial—it will determine whether DAT can cover its own leverage costs.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

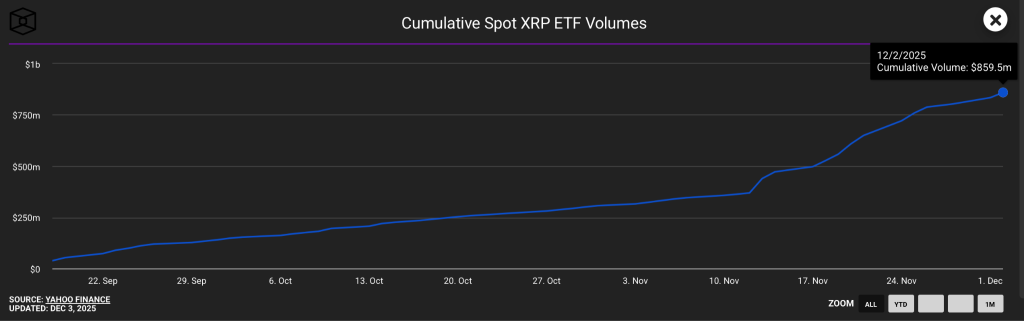

XRP ETF Flows Hit Record High—What It Means for XRP Price

Ethereum Hits New All-Time High for TPS Ahead of Fusaka Upgrade

Pi Network News: Expert Says ‘Sleeping Giant’ Fails to Wake As Stalled Protocol 23 Raises Doubts