Navigating the Illusion of Safety: Unmasking Value Traps in Japan's Bond Market

- Japan's BoJ ends YCC policy, triggering JGB market volatility and exposing structural risks. - Foreign investors shift to shorter-term JGBs amid liquidity concerns and rising yields. - High debt-to-GDP ratio and liquidity risks threaten Japan's fiscal stability and market resilience.

Japan's bond market has long been a magnet for foreign investors, lured by its reputation as a “safe haven” and the allure of yield in a world starved of returns. But in 2025, the cracks in this illusion are widening. The Bank of Japan's (BoJ) abrupt exit from its Yield Curve Control (YCC) policy in early 2024 has triggered a seismic shift in the JGB market, exposing structural vulnerabilities and creating a landscape rife with value traps. For investors, the challenge is no longer just about yield—it's about survival.

The Mirage of Safety: A Market in Transition

The BoJ's decision to abandon YCC marked the end of an era. For nearly a decade, the central bank had artificially suppressed long-term yields, capping the 10-year JGB yield near zero. This created a false sense of stability, masking the fragility of a market dominated by domestic buyers and reliant on central bank intervention. By August 2025, the 30-year JGB yield had climbed to 3.18%, nearly double the 10-year rate, as investors demanded compensation for duration risk.

The BoJ's tapering of JGB purchases—from ¥5.7 trillion monthly in August 2024 to ¥2.9 trillion by early 2026—has left the market vulnerable to supply shocks. Domestic life insurers, which hold 13% of outstanding JGBs, have offloaded ¥1.35 trillion in super-long bonds since October 2024, driven by mark-to-market losses and regulatory pressures. Meanwhile, foreign demand for long-maturity JGBs has plummeted by 67% in July 2025, as investors recalibrate to a new reality of higher volatility and liquidity constraints.

Structural Risks: The Hidden Costs of Fiscal Dependency

Japan's bond market is a house of cards built on fiscal dependency. With government debt-to-GDP exceeding 260%, the world's highest among developed economies, the country's ability to fund itself hinges on domestic buyers—particularly the BoJ, which owns 46% of outstanding JGBs. This dependency creates a dangerous feedback loop: as yields rise, the cost of servicing debt grows, forcing the government to issue more bonds, which in turn strains market liquidity.

The Ministry of Finance (MoF) has attempted to stabilize the market by shifting toward shorter-duration bonds, but this has only exacerbated imbalances in the super-long segment. The July 2025 20-year bond auction saw a bid-to-cover ratio of 3.15, below the 12-month average, signaling waning appetite. For foreign investors, the risk is clear: while Japan's fiscal fundamentals remain stable, the market's liquidity is increasingly fragile. A sudden selloff in the long-end could trigger a self-reinforcing spiral, akin to the UK's liability-driven investing (LDI) crisis in 2022.

The Foreign Investor's Dilemma: Yield vs. Liquidity

Foreign investors have poured ¥9.28 trillion into super-long JGBs in 2025, drawn by yields unseen in other developed markets. Yet this inflow masks a critical flaw: the market's liquidity is a mirage. The yen's 8% appreciation in 2025 has increased hedging costs, while Japan's aging population and shrinking workforce raise long-term fiscal concerns.

The recent unwinding of 10-year JGB positions by foreign investors—¥1.4 trillion in July 2025—reveals a growing awareness of these risks. Shorter maturities are now seen as a hedge against near-term volatility, including the July 2025 Upper House election and speculation about VAT cuts. This shift underscores a key lesson: in a maturity-driven market, duration is a double-edged sword.

A Strategic Framework: Differentiating Value from Illusion

For investors, the path forward requires a disciplined approach to risk. Here's how to navigate the traps:

Rebalance Duration Exposure: Avoid overconcentration in long-end JGBs. While the 30-year bond offers a 3.2% yield, its 22-year duration exposes portfolios to sharp price swings. Shorter maturities (e.g., 5–10 years) provide a buffer against volatility.

Hedge Currency Risk: The yen's strength has made JGBs less attractive for non-Japanese investors. Use forward contracts or currency ETFs to mitigate hedging costs.

Diversify Geographically: Japan's bond market is isolated. Pair JGBs with U.S. Treasuries or European bonds to reduce liquidity risk.

Monitor Policy Signals: The BoJ's potential recalibration of quantitative tightening (QT) in June 2025 could stabilize yields but may also reduce market depth. Watch for shifts in the BoJ's communication and auction results.

Leverage the GPIF: The Government Pension Investment Fund (GPIF) holds ¥250 trillion in assets and could reallocate toward super-long JGBs. Track GPIF's quarterly reports for clues on market support.

Conclusion: Repositioning for Resilience

Japan's bond market is at a crossroads. The BoJ's exit from YCC has unleashed forces that no central bank can fully control. For foreign investors, the lesson is clear: perceived safety is a trap. The market's structural risks—duration mismatch, fiscal dependency, and liquidity constraints—demand a strategic repositioning.

The time to act is now. By rebalancing duration, hedging currency exposure, and diversifying geographically, investors can preserve yield while mitigating the risks of a market in transition. In a world where certainty is an illusion, adaptability is the only true asset.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

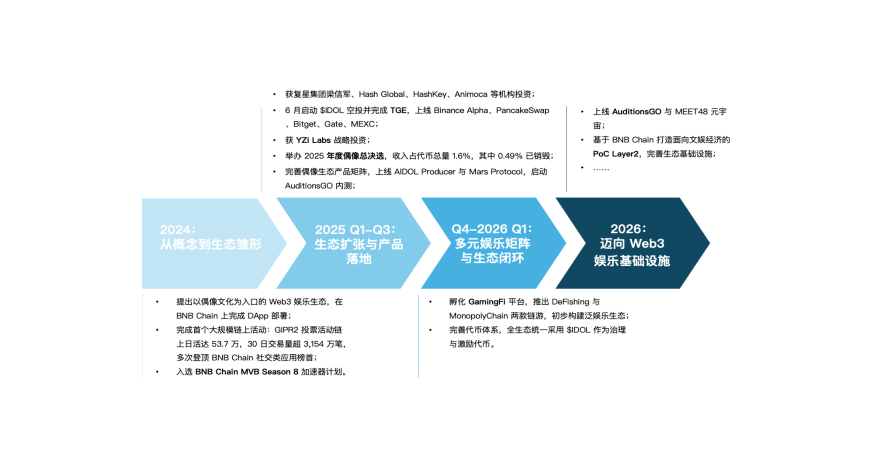

MEET48: From Star-Making Factory to On-Chain Netflix — How AIUGC and Web3 Are Reshaping the Entertainment Economy

Web3 entertainment is moving from the retreat of the bubble to a moment of restart. Projects represented by MEET48 are reshaping content production and value distribution paradigms through the integration of AI, Web3, and UGC technologies. They are building sustainable token economies, evolving from applications to infrastructure, aiming to become the "Netflix on-chain" and driving large-scale adoption of Web3 entertainment.

Digital Euro: Italy Advocates for a Gradual Implementation

Ethereum Validator Queues Surge as 2.45M ETH Sits in Exit Line

21Shares And Canary Ignite XRP ETF Approval Process